(Continuing from: Cisco Stock Valuation Analysis. Will CSCO Continue to Rise?)

- Technical Perspective

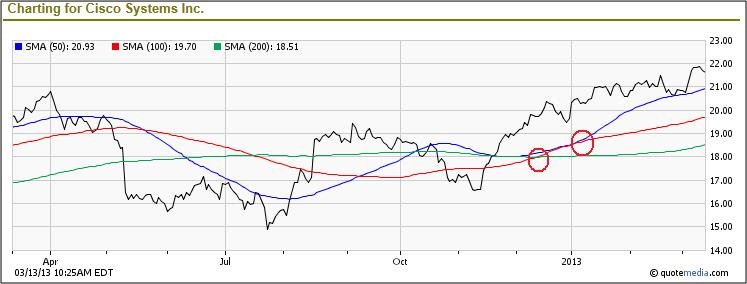

At the time of this analysis, CSCO is trading at $21.59 which, according to Morningstar data, is very close to the upper end of its 52-week trading range of between $14.96 and $21.98. Based on the 1 year stock movement chart below, it is clear that CSCO has had a downward trend for most of the first half of 2012. The stock recovered since late July 2012, and formed a strong base over the next several months, right up to the middle of Nov 2012. That base allowed to stock to find technical support at its 200-day Simple Moving Average (SMA), and set itself up for further upward momentum.

Towards the later part of Dec 2012, and into Jan 2013, CSCO exhibited two sets of Golden Cross movements (highlighted by red circles in the chart here), which saw the stocks shorter SMA's move above their longer-term values.

The Golden Cross is a classic signal that a stock has upward momentum, and CSCO has stayed true to that rule. Ever since late 2012, the stock has continued to move higher, finding strong support at its 50-day SMA ($20.93) on its way up. In the process, it is reaching to break out to new 52-week highs.

- Favorable Catalysts

Over the years Cisco has attained a reputation as being the de-facto vendor for network switches, routers and other enterprise level IT security and communications infrastructure for government departments and large corporations. The company's strong brand recognition, and excellent brand loyalty serves as a great catalyst to maintain existing customers and attract new ones.

By their very definition, Cisco products are not something that governments and corporations change every few months. Since they are high-end investments, most Cisco equipment are in place for at least 2 to 3 years. The high cost to quickly change and switch to another vendor is a catalyst that keeps many customers captive to Cisco.

Many companies have held back IT spending for the last 3 years or so because of economic uncertainty. However, with aging IT infrastructure taking its toll, and green shoots appearing in many economies, Cisco is well positioned to take advantage of this pent up demand.

Strong attempts by Cisco competitors, including HPQ, JNPR, ALU and BRCD, could mean that the company needs to constantly be vigilant about losing market share to innovative products. Additionally, low-cost competitors such as Chinese rival Huawei could force Cisco to compete on price, especially in lucrative emerging markets, driving its solid margins down.

The move by many multi-nationals to embrace the Cloud-computing model could mean that CSCO will face growing pressure from Cloud service providers to deliver other value-added services (such as a Software As A Service), for which CSCO is not yet fully prepared.

- Bottom Line Conclusion

Based on the above analysis, Cisco Systems would rate as a MODERATE BUY. However, it would be prudent to wait for a pullback on the stock before buying.

(By: Monty R. – MarketConsensus News Contributor)

Good luck in your investing. Let us know if you have any questions, comments or feedback,

MarketConsensus Stock Analysis Team

Stay In Touch:

Facebook (Like Us on Facebook)

Twitter (Follow Us on Twitter)

Google + (Connect with Us on Google+)

Contact Us (Questions/Comments)

Enter your e-mail address on the “Never miss a post!” section on the top right of this page and receive articles as soon as they are posted.

————————————————————————————————-

[related2][/related2]